Got some extra money sitting in your account? Before you spend it, put the numbers into this calculator and see exactly how much interest you could wipe out — and how many months off your loan you could buy.

Use the calculator below. Then read on if you want to understand what those numbers actually mean.

Loan Part Payment Calculator

What Is a Loan Part Payment?

A loan part payment (also called part prepayment) is a lump-sum amount you pay towards your loan over and above your regular EMI. It directly reduces your outstanding principal — which means less interest accumulates from that month forward, and your loan either ends sooner or your EMI drops.

It’s not the same as foreclosure (full payoff). You’re just paying extra — once, or occasionally — to shrink the debt faster.

Also useful: our Gold Loan Interest Calculator if you’re weighing whether to liquidate a gold investment for prepayment.

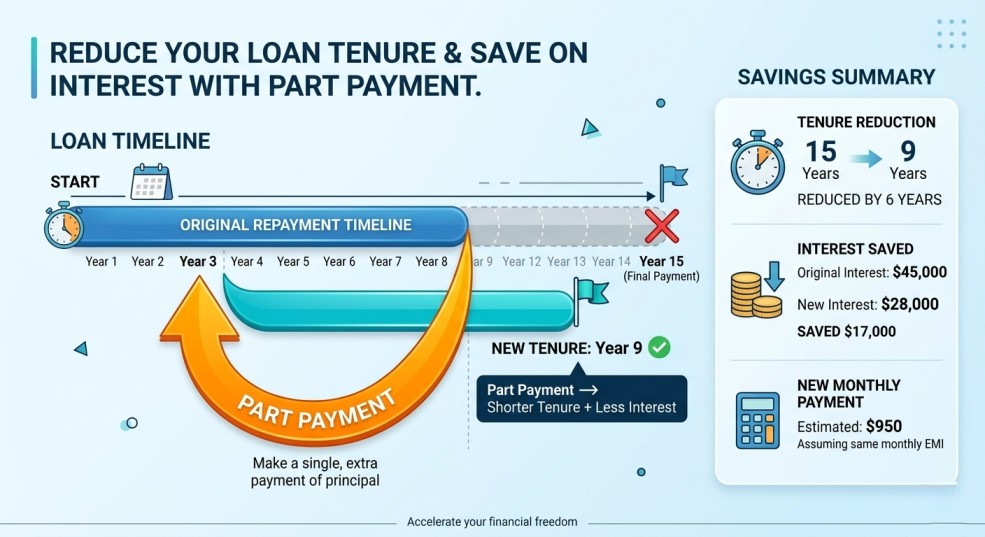

EMI Reduction vs Tenure Reduction — This Is the Decision That Actually Matters

Here’s the thing: when you make a part payment, your lender typically gives you a choice. You can either:

- Reduce your monthly EMI (keep the same end date, pay less each month), or

- Keep your EMI the same and reduce the tenure (end the loan earlier)

Most people pick EMI reduction because it feels like immediate relief. That’s understandable. But it’s usually the wrong call financially.

Why? Interest on a home loan accumulates over decades. The faster you shrink the principal, the less total interest you pay. Reducing tenure accelerates that shrinkage. Reducing EMI just makes your monthly life easier while the bank collects more interest overall.

If your monthly cash flow is comfortable, always choose tenure reduction. The savings are significantly higher.

Option 1: Reduce EMI | Option 2: Reduce Tenure |

|---|---|

Monthly Payment: This option lowers your monthly installment, giving you more “breathing room” and extra cash in your pocket every month. | Monthly Payment: Your monthly installment remains exactly the same as before. You continue paying the same amount to the bank. |

Total Interest Saved: You will save a moderate amount of interest. While helpful, it is not the most cost-effective way to handle a prepayment. | Total Interest Saved: This allows for maximum savings. You aggressively cut down the interest the bank charges you over the life of the loan. |

Time to Debt-Free: Your loan will end on the same original date. You aren’t finishing the loan faster; you are just paying less per month. | Time to Debt-Free: You will become debt-free much earlier. This path significantly shortens the number of months left on your loan. |

Best For: Ideal for individuals with a tight monthly budget who need to manage their day-to-day cash flow more easily. | Best For: Ideal for those focused on maximum savings and long-term wealth building by eliminating debt as fast as possible. |

Recommended if… You should choose this if your cash flow is strained or if you have new monthly expenses that make the current EMI hard to pay. | Recommended if… You should choose this if you are financially stable and can comfortably afford your current monthly payments without stress. |

How to Use This Loan Part Payment Calculator

No sign-up. No app. Just enter four numbers and get your answer instantly.

- Step 1: Enter your current outstanding loan amount (what you still owe today).

- Step 2: Enter your interest rate per year.

- Step 3: Enter the remaining tenure in years.

- Step 4: Enter the part payment amount you’re planning to make.

- Step 5: Select your currency — ₹ Indian Rupee or $ US Dollar.

- Step 6: Hit Calculate. You’ll instantly see your new tenure, interest saved, and monthly EMI.

Real Example: How Much Can You Actually Save?

Scenario: Home Loan (INR)

- Loan Amount: ₹40,00,000 | Rate: 8.5% | Tenure: 18 years | Part Payment: ₹3,00,000

Scenario 1: Without Part Payment | Scenario 2: With Part Payment |

|---|---|

Monthly EMI: You continue to pay your standard amount of ₹34,844 every month until the end of the loan period. | Monthly EMI: Your payment remains ₹34,844 (unchanged). Even after paying a lump sum, your monthly commitment stays the same. |

Total Interest: Over the full life of the loan, you will pay a total of ₹35,09,968 in interest charges to the bank. | Total Interest: Because you paid a portion of the principal early, your total interest drops to ₹29,64,312. |

Interest Saved: In this scenario, there is no interest saving. You pay the maximum amount of interest according to your original schedule. | Interest Saved: By making a part payment, you successfully save ₹5,45,656 that would have otherwise gone to the bank. |

Remaining Tenure: You are committed to the bank for the full remaining duration of 216 months. | Remaining Tenure: Your loan duration is slashed down to approximately 181 months, significantly shortening your debt journey. |

Months Cut: There is no reduction in the time you spend paying off the loan. | Months Cut: You save approximately 35 months, meaning you become debt-free almost 3 years earlier than planned. |

One payment of ₹3 lakh saves you ₹5.45 lakh in interest. That’s a 1.8x return on your lump sum — guaranteed.

Scenario: Personal Loan (USD)

- Loan Amount: $15,000 | Rate: 12% | Tenure: 4 years | Part Payment: $2,000

Scenario 1: Without Part Payment | Scenario 2: With Part Payment |

|---|---|

Monthly EMI: Your monthly installment remains at $395. You continue to pay this fixed amount according to your original loan schedule. | Monthly EMI: Your monthly payment stays exactly the same at $395. The part payment does not lower your monthly bill, but it works behind the scenes. |

Total Interest: Under the original plan, you will pay a total of $3,950 in interest charges over the remaining life of the loan. | Total Interest: By paying a lump sum now, your total interest cost is reduced to $3,140, making your loan much cheaper overall. |

Interest Saved: There is no interest bachat here. You will pay the full amount of interest as calculated by the bank at the start. | Interest Saved: This is the big benefit; you successfully save approximately $810 in interest that you no longer owe to the bank. |

Months Cut: Your loan duration does not change. You will keep paying for the full remaining term without any time saved. | Months Cut: You finish your loan much faster. You cut approximately 5 months off your schedule, becoming debt-free sooner. |

When Is the Best Time to Make a Part Payment?

The earlier you make a part payment, the greater the impact. In the first few years, a massive portion of each EMI goes toward interest.

Timing Impact (₹50 Lakh Home Loan @ 8.5% for 20 years, ₹5 Lakh Part Payment):

Early Payment (Year 1 – 5) | Late Payment (Year 10 – 15) |

|---|---|

Year 1 Impact: Making a payment at the very start is the most powerful. You save a massive ~₹9.8 lakh in interest and cut your tenure by ~4.5 years. | Year 10 Impact: By the halfway mark, the impact reduces. You still save ~₹3.1 lakh in interest and shorten your loan by ~1.8 years. |

Year 5 Impact: Paying at this stage is still very effective. You save roughly ~₹6.2 lakh and get out of your debt ~3.1 years earlier than planned. | Year 15 Impact: At this late stage, most interest is already paid. You save only ~₹0.9 lakh and reduce your time by about 7 months. |

The Advantage: Early payments attack the principal balance when it is highest, preventing interest from compounding over decades. | The Reality: As the loan nears the end, your payments go mostly toward the principal anyway, so the “bonus” of a part-payment is much lower. |

Strategy: Focus on making extra payments as soon as possible to get the Maximum Financial Benefit. | Strategy: While still helpful, late payments are more about closing the file rather than saving huge amounts of money. |

The Expert Insight: Most people think it doesn’t matter when they pay. Actually, the difference between Year 1 and Year 15 is a massive ₹9 lakh in savings. The earlier, the better.

Prepayment Charges — Don’t Forget This Before You Calculate

As per Reserve Bank of India (RBI) guidelines, banks cannot levy pre-closure charges on floating-rate personal loans for individuals.

- Floating rate home loan? No penalty.

- Fixed rate personal loan? Check for 1%–5% charges.

- NBFC loan? Rules may vary, check your contract.RBI’s official guidelines on foreclosure charges

The ToolzyWorld Expert Tip: Tax vs. Savings

Before you wipe out your loan, remember that Home Loan interest often gives you tax benefits (like Section 24 in India). If your interest rate is low and your tax bracket is high, you might actually save more by keeping the loan and investing that lump sum elsewhere. However, for most people, the Psychological Win of being debt-free outweighs the minor tax savings. Peace of mind is the best ROI.

Voice Search Q&A (FAQs)

Q: What is a loan part payment calculator?

A: It’s a free tool that shows how much interest you’ll save and how many months your loan will be cut short when you pay an extra lump sum.

Q: Is it better to reduce EMI or tenure?

A: Always reduce tenure for maximum interest savings. Reduce EMI only if you are facing a month-on-month cash crunch.

Q: Does part payment reduce EMI automatically?

A: No. You must specify to your bank whether you want to reduce the monthly EMI or the remaining time (tenure).

Q: Are there charges for home loan part payment in India?

A: For floating-rate loans, there are zero charges as per RBI. For fixed-rate loans, check for a 2-5% penalty.